At its core, EasyCash is a loan that sits inside your credit card.

Instead of using your card to buy something, you request cash. Once approved, the amount is credited to your account, and you repay it over time with interest.

What makes it different from a regular cash advance is structure. A cash advance starts charging high interest immediately and doesn’t guide you into fixed payments. EasyCash, on the other hand, spreads your repayment into predictable monthly installments.

That predictability is the main reason people choose it, especially for planned expenses.

Let’s break it down properly.

- Who can actually use it

- Key Information: UB EasyCash at a Glance

- How much you can borrow in real terms

- Interest and fees in plain language

- How the money actually reaches you

- Understanding repayment without the jargon

- Why your minimum due can mislead you

- What happens if you don’t pay in full

- Ending your installment early

- What people actually experience using EasyCash

- When it actually makes sense to use

- Final Thoughts

Who can actually use it

UnionBank doesn’t make this available to everyone automatically. You need to be a cardholder in good standing, and even then, approval isn’t guaranteed.

In practice, most mainstream UnionBank credit cards are eligible, including rewards, cashback, miles, and co-branded cards. But availability can vary per account, which is why many users only see the offer inside the app when they qualify.

If you don’t see it in your app, it doesn’t always mean you’re permanently ineligible. Sometimes it just means you’re not currently pre-approved.

Key Information: UB EasyCash at a Glance

| What it is | Credit card-to-cash installment facility that converts a portion of your UnionBank credit limit into cash, payable in fixed monthly installments with interest |

| How to access | Via UnionBank Online, customer service hotline at (+632) 8981-4700, or pre-approved SMS/email offers |

| Maximum amount | Up to 100% of available credit limit |

| Processing fee | ₱900 per approved EasyCash transaction (non-refundable) |

| Interest rate | Around 1% monthly add-on rate (varies per offer); fixed for the entire term; estimated ~22%–24% annual effective rate |

| Repayment structure | Fixed monthly installment including principal and interest, computed on a diminishing balance basis |

| Available terms | 6 to 60 months |

| Disbursement speed | Instant for UB accounts, 3-5 days for other banks |

| Where funds are sent | Credited to a nominated bank account under the cardholder’s name (UnionBank accounts are usually faster) |

| Impact on credit limit | Approved amount is deducted from available credit limit and gradually restored as principal is paid |

| Early repayment | Allowed anytime, subject to pre-termination fee and accrued interest charges |

| Rewards eligibility | Not eligible for points, miles, or cashback |

| Purpose / use | Can be used for any personal financial need without restriction |

How much you can borrow in real terms

This is where expectations and reality can differ.

You’re not borrowing based on your total credit limit. You’re borrowing from what’s left after your current balance.

For example, if you have a ₱100,000 limit but already used ₱30,000, your available credit is ₱70,000. From that, you can typically borrow up to around 80 percent, so roughly ₱56,000.

There’s also a minimum amount required to avail, usually starting at ₱3,000.

What’s important here is that approval isn’t always equal to your requested amount. The bank can approve less depending on your credit profile.

Interest and fees in plain language

UnionBank presents interest using something called a monthly factor rate, often around 1 percent per month in sample scenarios.

But what really matters is the effective annual rate, which ends up somewhere in the low to mid 20 percent range per year when everything is factored in.

On top of that, there’s a one-time processing fee. Depending on your card type, it’s usually around ₱350 for most cards, though some premium cards are charged higher.

The key thing to understand is that this fee is charged upfront and isn’t refundable, even if you cancel early.

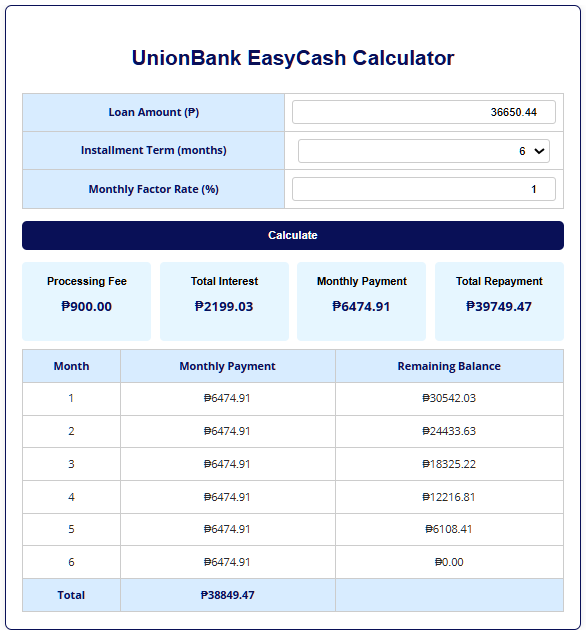

Access the UnionBank EasyCash calculator here.

How the money actually reaches you

Once approved, the process feels surprisingly straightforward.

Most people receive the funds directly in their bank account. If you’re using a UnionBank account and applying through the app, it can arrive instantly. Transfers to other banks usually take a bit longer, around three to five banking days.

There’s also an option for a manager’s check if you apply through customer service, but in practice, most users prefer direct transfers because it’s faster and more convenient.

From real user experiences, the app-based process is usually the smoothest. It removes a lot of the friction you’d expect from a traditional loan.

Understanding repayment without the jargon

You choose a term, typically anywhere from 6 months up to 60 months. Your total amount, including interest, is divided into fixed monthly installments.

At first glance, that sounds simple. But the billing flow has a small twist that catches a lot of people off guard. Your first statement doesn’t show your monthly installment yet. Instead, it shows something called initial interest. This is the interest calculated from the day your loan was approved up to your first billing cut-off.

Your actual monthly installment only starts appearing in your second statement. That gap is one of the most common sources of confusion, especially for first-time users who expect immediate installment billing.

Why your minimum due can mislead you

This is one of the biggest traps, and it’s not obvious unless you look closely. Your statement will show a Minimum Amount Due, but it’s not equal to your monthly installment.

Instead, it’s calculated differently and ends up much smaller than what you actually need to pay to stay on track. In simple terms, your minimum due includes:

- All of the interest for the month

- A small portion of the principal

- A small percentage of the remaining balance

Because of this, many users think they’re safe paying just the minimum. In reality, doing that can stretch your balance longer and trigger additional interest charges.

If you want to avoid extra costs, you need to pay your full statement balance, not just the minimum.

What happens if you don’t pay in full

Once you miss paying the full amount due, the situation changes.

Your remaining balance starts getting charged with the regular retail interest rate, which is significantly higher than your installment rate. This interest is computed daily and compounded monthly.

Over time, this can erase the main advantage of EasyCash, which is controlled and predictable repayment.

If the account becomes severely overdue, the bank can cancel the installment entirely and require you to pay the remaining balance in full.

Ending your installment early

You’re not locked in forever, but getting out early isn’t completely free.

UnionBank allows early repayment, but you’ll need to settle the remaining balance plus a cancellation fee, typically a percentage of the remaining principal.

There’s also a short cooling-off period, usually at least two banking days, where you can cancel after availing. But even then, some fees and interest may still apply depending on timing.

So while flexibility exists, it comes with a cost.

What people actually experience using EasyCash

Looking at real user feedback, EasyCash is often described as convenient but easy to misunderstand.

Many users like it because it’s fast and doesn’t require a separate loan application. The structured payments also make it easier to plan compared to revolving credit card balances.

At the same time, common issues tend to revolve around expectations.

Some users are surprised by the first billing cycle. Others underestimate how much interest they’ll pay over longer terms. And a lot of people initially think the minimum due is enough, which leads to higher costs later.

The pattern is clear. The product works well when you understand it fully, but becomes expensive when used casually.

When it actually makes sense to use

EasyCash is most useful when you already know exactly how you’ll repay it.

It works well for planned expenses where you need cash instead of card payments, and where spreading payments over several months helps your cash flow.

It’s less ideal for uncertain situations or long-term borrowing, especially if you’re not confident about paying the full amount due every month.

Final Thoughts

UnionBank EasyCash isn’t complicated, but it does require attention to detail.

It’s a structured loan disguised as a credit card feature. If you treat it like a proper loan with fixed payments, it can be useful. If you treat it like a flexible credit line and rely on minimum payments, it can become expensive quickly.

The difference comes down to how well you understand the billing and how disciplined you are with repayment.

Turning Credit Limit to Cash Collections

Explore Credit Cards By Bank