If you have an EastWest credit card, chances are you’ve seen offers for InstaCash, sometimes via text, email, or inside the ESTA chatbot.

At first glance, it sounds simple. You just convert your credit limit into cash and pay it monthly. But once you look closer, the questions start coming in:

- How much will it really cost?

- Is it better than a cash advance?

- And is it actually a good idea to use it?

This guide breaks it all down in a way that actually makes sense, based on both official terms and real user experiences.

- What EastWest InstaCash Actually Is

- Key Information: EastWest InstaCash at a Glance

- How the Process Feels in Real Life

- The Interest Rate (Where Things Get Important)

- Fees You Might Overlook

- How It Compares to a Regular Cash Advance

- What Real Users Say (That Banks Don’t Tell You)

- When InstaCash Makes Sense

- The Part Most People Underestimate

- Final Thoughts

What EastWest InstaCash Actually Is

In simple terms, InstaCash lets you borrow against your credit card limit and receive the money in cash.

Instead of swiping your card for purchases, you’re essentially taking out a loan. The amount you borrow is deducted from your available credit limit, and you pay it back in fixed monthly installments.

If you’ve ever used installment plans on your card, it works in a very similar way, except this time, the money goes straight to your bank account.

Key Information: EastWest InstaCash at a Glance

| What it is | Credit card-to-cash installment feature (convert part of your EastWest credit limit into cash) |

| How to access | Available via ESTA chatbot, hotline, or targeted offers (SMS/email) for eligible cardholders |

| Minimum amount | ₱10,000 (may vary per offer) |

| Maximum amount | Depends on your available credit limit and bank approval |

| Processing fee | – ₱500 (via ESTA/online) – ₱1,000 (via agent/hotline) |

| Interest rate | – Monthly add-on rate (commonly ~0.3% to 1%, depending on offer) – Fixed for the entire term – Longer terms tend to have slightly lower interest rate |

| Repayment structure | – Fixed monthly installment – Amount and duration are set upon approval |

| Available terms | Usually 6 to 60 months (varies per offer) |

| Disbursement speed | Typically within 3 to 10 banking days after approval |

| Where funds are sent | Any nominated local bank account under your name |

| Impact on credit limit | Approved amount is deducted from your available credit limit |

| Early repayment | – Pre-termination allowed – Subject to pre-termination fee (based on remaining balance or minimum fee) |

| Rewards eligibility | Not eligible for rewards points, miles, or cashback |

| Purpose/use | Can be used for any purpose (no need to declare usage) |

How the Process Feels in Real Life

The application itself is usually straightforward. Most people go through EastWest’s ESTA chatbot, though some apply via hotline or targeted offers.

Once you apply, the bank evaluates your request. If approved, the funds are deposited into your nominated account. Based on user experiences, this typically takes anywhere from a few days to about a week, though it can stretch a bit longer in some cases.

After that, the repayment just shows up in your monthly credit card statement. You don’t need to manage a separate loan account, which is one of the reasons people find it convenient.

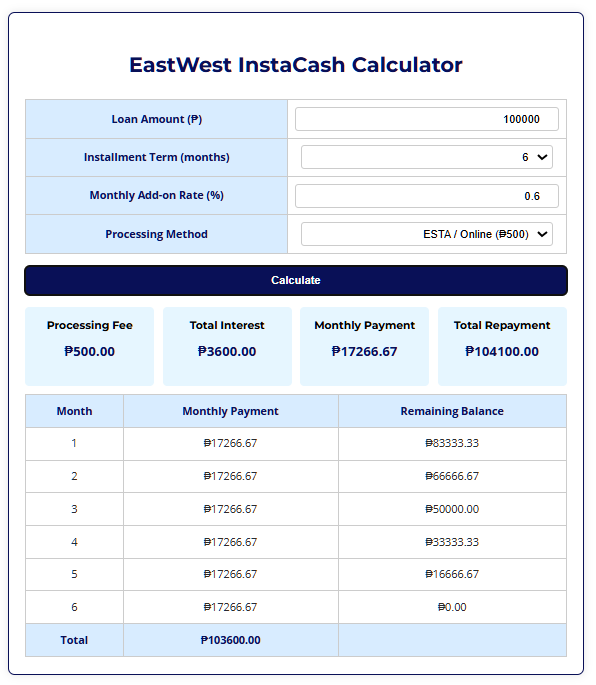

The Interest Rate (Where Things Get Important)

This is the part that matters most, and also the part that confuses a lot of people.

EastWest doesn’t publish a single fixed rate for InstaCash. Instead, the interest is usually presented as a monthly add-on rate, and it varies depending on your profile and the offer you receive.

From actual users, rates commonly fall somewhere between 0.3% to 1% per month. That might sound low, but here’s the catch. Add-on rates are not the same as regular interest rates.

Even a “small” monthly rate can translate to a significantly higher effective cost over time. That’s why two people can have very different opinions about InstaCash, one sees it as cheap, another feels it’s expensive.

Access the EastWest InstaCash calculator here.

Fees You Might Overlook

Aside from interest, there’s also a processing fee, typically ₱500 to ₱1,000 depending on how you apply. This is easy to ignore, but it matters especially for smaller loan amounts. In some cases, it’s charged upfront; in others, it’s rolled into the loan.

It won’t make or break the decision, but it’s something you should factor into the total cost.

How It Compares to a Regular Cash Advance

If you’re deciding between InstaCash and a standard credit card cash advance, the difference is pretty clear once you look at the structure. A cash advance starts charging high interest almost immediately and doesn’t come with structured repayment. It’s flexible, but expensive and easy to spiral.

InstaCash, on the other hand, spreads payments over time with a fixed monthly amount. Because of that, it’s generally much cheaper and easier to manage, especially for larger amounts.

That’s why most people who understand both options will choose InstaCash over a straight cash advance almost every time.

What Real Users Say (That Banks Don’t Tell You)

This is where things get interesting, because actual experiences don’t always match the clean, official explanation.

Some users report getting very competitive rates, sometimes even below 0.6% monthly, especially if they have a good history with the bank. Others receive higher offers closer to 1%, which can feel less attractive compared to other banks.

Another common experience is that not everyone gets the option right away. InstaCash is often tied to pre-approved offers, so availability can depend on how you use your card.

Processing time also varies. While some people receive funds within a few days, others mention waiting closer to 7–10 banking days. It’s not instant, so it’s not ideal for urgent, same-day needs.

And interestingly, people don’t just use it for emergencies. Some use it for big planned expenses, things like home improvements, tuition, or even property-related payments. That flexibility is part of its appeal, but it also makes it easy to justify borrowing when you don’t really need to.

When InstaCash Makes Sense

InstaCash works best when there’s a clear reason behind the loan.

If you’re dealing with an emergency, consolidating higher-interest debt, or funding something important that you’ve already planned for, it can be a practical option. The structured payments and relatively lower rates (compared to cash advance) make it manageable.

Where it becomes risky is when it’s used casually, just because the credit is available. Since the money comes from your card, it doesn’t always feel like a traditional loan, and that can lead to overborrowing.

The Part Most People Underestimate

The biggest mistake people make with InstaCash isn’t the interest rate, it’s underestimating the commitment.

Once you take it, you’re locking yourself into monthly payments for several months or even years. That reduces your available credit and adds a fixed obligation to your budget.

So before applying, the better question isn’t just “Can I afford the monthly?” Instead, you need to ask, “Will this still feel manageable 6–12 months from now?“

Final Thoughts

EastWest InstaCash is one of the more convenient ways to access cash using your credit card. It’s easier than applying for a personal loan, and usually cheaper than a cash advance.

But convenience cuts both ways. It makes borrowing easier, which also means it’s easier to misuse.

If you treat it like a structured loan with a clear purpose, it can be genuinely useful. If you treat it like extra spending money, it can quietly become a burden.

Looking for other credit-to-cash options? Check out these articles.

Turning Credit Limit to Cash Collections

Explore Credit Cards By Bank