If you’ve ever looked at your credit card limit and thought, “I wish I could just turn this into cash,” that’s exactly what BPI Credit to Cash allows you to do.

Instead of swiping your card at a store, you’re essentially borrowing against your credit limit and having the money deposited straight into your bank account. No separate loan application, no long approval process, just a conversion of credit into usable cash.

It sounds simple (and it is), but the details matter. A lot of cardholders jump in thinking it’s “cheap” because of the low monthly rate, only to realize later that the total cost adds up.

Let’s break it down properly.

- So What Is BPI Credit to Cash, Really?

- Key Information: BPI Credit to Cash at a Glance

- How the Process Feels in Real Life

- The Interest Rate (Where Things Get Important)

- Fees You Might Overlook

- What Borrowing Actually Looks Like

- BPI Credit to Cash Real User Experience

- When It Makes Sense to Use Credit to Cash

- Credit to Cash vs Cash Advance (A Quick Reality Check)

- A Few Practical Tips Before You Apply

- Final Thoughts

So What Is BPI Credit to Cash, Really?

At its core, BPI Credit to Cash is just an installment loan tied to your credit card.

When you avail of it, BPI takes a portion (or even all) of your available credit limit and converts that into cash. That amount gets deposited into your chosen bank account, and in return, you agree to pay it back over a fixed number of months.

It behaves a lot like buying something on installment, except this time, the “purchase” is cash itself.

One important thing to understand early: the moment your loan is approved, your credit limit drops by the same amount. If you borrow ₱50,000, that’s ₱50,000 less available for spending on your card.

Key Information: BPI Credit to Cash at a Glance

| What it is | Credit card-to-cash installment feature (convert part of your BPI credit limit into cash) |

| How to access | Available via BPI hotline, branch, or targeted offers (SMS/email); sometimes visible in the BPI app for selected users |

| Minimum amount | ₱3,000 |

| Maximum amount | Up to 100% of your available credit limit (subject to approval) |

| Processing fee | – ₱300 (for lower loan amounts) – ₱500 (for higher loan amounts) |

| Interest rate | – As low as 0.39% to 1% monthly add-on rate – Fixed for the entire term – Promo rates may be lower for selected users |

| Repayment structure | – Fixed monthly installment – Amount and duration are locked in upon approval |

| Available terms | 6 to 60 months |

| Disbursement speed | Typically within 3 to 5 banking days after approval |

| Where funds are sent | Any nominated local bank account (usually under your name) |

| Impact on credit limit | – Approved amount is deducted from your available credit limit – Madness limit can also be utilized |

| Early repayment | – Pre-termination allowed – Subject to pre-termination fee |

| Rewards eligibility | Not eligible for rewards points, miles, or cashback |

| Purpose/use | Can be used for any purpose (no need to declare usage) |

How the Process Feels in Real Life

In practice, most people don’t go through a complicated application process.

Some get a text or email offer from BPI. Others call the hotline or ask at a branch. If you’re eligible, approval can be surprisingly quick, and many users report receiving the money within a few days.

From real user experiences online, a common timeline looks like this:

- Application or confirmation of offer

- Approval within a few days

- Funds credited in about 3–5 banking days

It’s not instant, but it’s fast enough for planned expenses.

The Interest Rate (Where Things Get Important)

This is where most of the confusion happens.

BPI usually advertises Credit to Cash at around 0.39% to 1% per month add-on rate. At first glance, that sounds low, especially compared to other loans or credit card charges.

But that interest rate is not the same as a typical interest rate you see in savings or personal loans. It’s an “add-on” rate, which means the interest is calculated upfront based on the original loan amount, not the remaining balance.

When you convert that into a more realistic yearly cost, it’s closer to 10% to 21% effective interest per year.

That’s still significantly cheaper than a credit card cash advance (which can hit 3% per month and compounds), but it’s not exactly cheap money either.

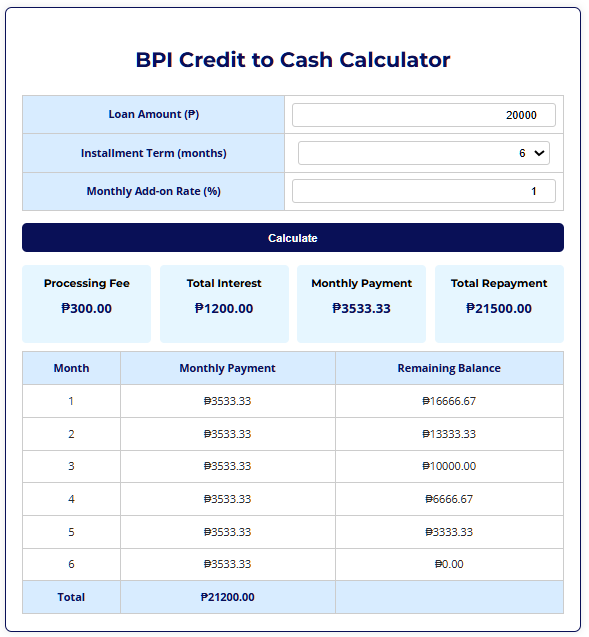

Access the BPI Credit to Cash calculator here.

Fees You Might Overlook

Aside from interest, there’s also a processing fee of ₱300. It’s a one-time charge, but it still adds to your total cost.

There’s also something many people don’t expect: if you decide to pay off the loan early, BPI may charge a pre-termination fee. So even if you suddenly have the money to settle everything, it’s not always free to exit early.

These are small details individually, but together they affect how “worth it” the loan really is.

What Borrowing Actually Looks Like

Let’s make this more concrete.

Say you borrow ₱20,000 over 12 months at around 1% monthly add-on. Your monthly payment might look manageable, but by the time you finish paying everything, you’ve added several thousand pesos in interest and fees. That’s why focusing only on the monthly payment can be misleading.

The better question is always: How much am I paying in total?

For the example given above, your monthly amortization would be ₱1,866.67. This totals to an interest of ₱2,400 for the 12-month term. That’s a fair interest if the loan is put into good use, business, or an emergency.

BPI Credit to Cash Real User Experience

If you look at online discussions, especially in local finance communities, the sentiment is pretty consistent.

People like how easy and accessible it is. It’s often described as one of the fastest ways to get cash without dealing with traditional loan requirements.

At the same time, there’s a recurring realization: once you compute the total repayment, it feels more expensive than expected.

Some users also mention that:

- The feature isn’t always visible in the app unless you’re pre-selected

- Promo rates (lower than 1%) sometimes exist but aren’t guaranteed

- Approval is easier if you already have a good history with your card

In short, it’s convenient, but not something people recommend using casually.

When It Makes Sense to Use Credit to Cash

This kind of loan works best when the need is clear and planned.

For example, it can make sense if you’re dealing with a large, unavoidable expense like medical bills, tuition, or even short-term business capital. In those situations, having structured monthly payments is better than letting credit card interest spiral out of control.

Where it becomes risky is when it’s used for lifestyle spending or things that don’t really need financing. Turning your credit limit into cash can feel easy, but that’s exactly why it’s easy to overuse.

Credit to Cash vs Cash Advance (A Quick Reality Check)

If your alternative is a credit card cash advance, then Credit to Cash is almost always the better option.

Cash advances start charging interest immediately, at much higher rates, and they compound quickly. In comparison, Credit to Cash gives you fixed payments and a lower overall cost.

But that doesn’t automatically make it a “good” deal, it just makes it the less expensive option between two costly choices.

A Few Practical Tips Before You Apply

If you’re considering it, it’s worth slowing down just a bit and doing a few simple checks.

First, see if you have a promo offer. Some cardholders get significantly lower rates, and that can make a big difference.

Second, check if you have access to a Madness Limit, which is a special credit line that doesn’t reduce your regular limit. Not everyone has it, but if you do, it’s a big advantage.

And finally, always compute the total repayment. Not just the monthly amount, not just the interest rate, the full amount you’ll pay from start to finish.

Final Thoughts

BPI Credit to Cash sits in a very practical middle ground.

It’s not as strict or complicated as a personal loan, and it’s far safer than relying on cash advances. That’s why so many Filipinos end up using it at some point.

But convenience can be misleading. The ease of access makes it feel light, when in reality, it’s still a fairly expensive form of borrowing. Used intentionally, it’s a helpful tool. Used casually, it can quietly add to your debt faster than you expect.

Turning Credit Limit to Cash Collections

Explore Credit Cards By Bank