SPayLater, LazPayLater, BillEase, and Atome all let you split a purchase into installments, but very few of them publish an exact interest rate for every term. This guide walks through what each one actually discloses, what stays unknown until you check your own offer, and a calculator that works both ways: a quick typical-range estimate, and a precise calculation once you have your real rate.

If you’ve compared BNPL apps side by side, you’ve probably noticed the published numbers don’t always match what shows up at your own checkout. That’s not a mistake on your end. Most of these providers quote a range (say, 1 to 5% interest) rather than a fixed rate, and the exact figure you get depends on your account, the merchant, and sometimes the specific item. This article breaks down what’s actually known about each provider, and gives you a tool to calculate your real cost once you have your personal offer in hand.

What Is BNPL and How Does It Work in the Philippines?

BNPL (buy now, pay later) lets you take an item home today and pay for it over several weeks or months, usually without needing a credit card. In the Philippines, the apps you’ll run into most at checkout are SPayLater (Shopee), LazPayLater (Lazada), BillEase, and Atome.

Here’s where people get confused: BNPL feels free because there’s often a “0% interest” option somewhere in the app. In simple terms, that 0% usually only applies to a specific short window, like a 40-day pay-in-full option, or to select merchants running a promo. Once you move to a multi-month installment plan, interest and fees usually apply, and the exact figure is something each provider determines per user rather than publishing as one fixed rate. Note that this article shows you the full published range for each provider, and gives you a calculator for once you know your own exact rate.

SPayLater (Shopee)

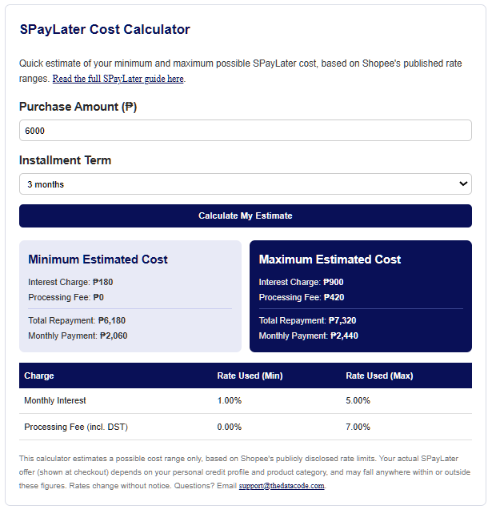

SPayLater publishes a range rather than a fixed number: interest of 1 to 5% per month, plus a processing fee of 0 to 7% (this includes documentary stamp tax, a small government fee added to loan documents). Your plan can run up to 12 months, and a late payment adds 2.5 to 5% on the overdue amount.

Where you land in that range depends on your Shopee account history, the merchant, and the specific installment term you pick at checkout. There’s no public table mapping “6 months equals X%,” so the most reliable number is always the one shown to you in-app right before you confirm.

LazPayLater (Lazada)

LazPayLater’s interest also falls in a 1 to 5% per month range, similar to SPayLater, with plans available up to 12 months. Where it differs is the fee structure: instead of a percentage-based processing fee, LazPayLater charges a flat PHP1.50 for every PHP200 you finance (which works out to 0.75% of your loan amount, a fixed and predictable amount unlike the interest portion). Late payments are charged at 5% of the overdue amount or PHP50, whichever is higher.

Let’s say you’re financing ₱10,000. The fee portion alone is predictable: ₱75 (0.75% of ₱10,000). The interest portion still depends on your specific offer, somewhere between ₱100 and ₱500 per month depending on where you land in the 1 to 5% range.

BillEase: Pay with Grace vs Regular Installments

BillEase actually has two distinct paths, and they shouldn’t be averaged together since the cost difference between them is significant.

Pay with Grace is BillEase’s 0% interest option, available on eligible merchants for 3 or 6 month terms. If your purchase qualifies, you pay exactly the sticker price spread across the term, nothing more.

Regular installments apply once you’re outside Pay with Grace eligibility, or choosing a longer term. BillEase discloses a flat 3.49% interest per month here, applied to the term you select. Unlike SPayLater or LazPayLater, this is one of the few rates in this comparison that’s actually published as a single fixed number rather than a range, though note that BillEase’s own in-app sample computations have, in our checks, not always matched a simple flat 3.49%-per-month formula exactly. Treat the number here as the best published baseline, and confirm your specific total in-app before committing.

Atome

Atome’s clearest published term is its 0% interest option for purchases paid in full within 40 days. Beyond that window, if you move to a multi-month installment plan (Atome offers plans up to 6 months), the regular interest rate is not publicly disclosed anywhere we could find; no fee schedule, no rate table, nothing in the public terms.

This means if you’re considering Atome for a multi-month plan rather than the 40-day option, the only reliable way to know your real cost is to check the exact figure Atome shows you at checkout. We’ve left this clearly marked as “rate not disclosed” in the calculator below rather than guessing.

Fees at a Glance

| Provider | Interest | Other fees | Max term | Late fee |

|---|---|---|---|---|

| SPayLater | 1 to 5% per month | Processing fee 0 to 7% (incl. DST) | 12 mo | 2.5 to 5% |

| LazPayLater | 1 to 5% per month | PHP1.50 per PHP200 financed | 12 mo | 5% or PHP50, whichever is higher |

| BillEase (Pay with Grace) | 0% (eligible merchants, 3 to 6 mo) | None | 6 mo | Varies |

| BillEase (Regular) | 3.49% per month (published baseline) | None | Up to 12 mo | Varies |

| Atome | 0% up to 40 days; not disclosed beyond that | Not disclosed | 6 mo | Not disclosed |

BNPL Cost Calculator

This tool works in two parts. The first gives you a typical-range estimate based on each provider’s published rates. The second lets you plug in the exact rate from your own in-app offer for a precise number. Use the first to compare providers broadly, and the second once you actually have an offer in hand.

Part 1: Typical Range Estimate

These are estimates only, based on each provider’s published rate range. They are not a quote and may not match your personal offer.

Part 2: Calculate Your Exact Cost

Already have your offer? Enter your purchase amount, term, and the exact interest rate and fee shown in your app for a precise total.

Leave the rate or fee field blank to treat it as 0%. Rates and policies may change without notice. Questions? Email support@thedatacode.com.

How to Use the Calculator

- Start with Part 1 to see a typical range across all providers for your purchase amount and term. This gives you a rough sense of where each one tends to land.

- Check your actual offer in-app. Open SPayLater, LazPayLater, BillEase, or Atome and see what specific rate or fee they quote you for your real purchase.

- Use Part 2 with that real number. Enter your purchase amount, term, and the exact interest rate and fee you were shown for a precise total, not an estimate.

- If you don’t have a fee figure to enter, leave that field blank. The calculator will tell you what it assumed (0% for any blank field) so you’re not misled by a number that looks more precise than it is.

Things to Watch Out For

- “0% interest” usually has conditions. It often only applies to specific merchants, shorter terms, or a pay-in-full window like Atome’s 40 days, read the fine print before assuming every purchase qualifies.

- Late fees add up fast. Most of these charge 2.5 to 5% per month (or a flat ₱50, in LazPayLater’s case) on overdue amounts, a much higher effective rate than the financing itself, so set a payment reminder.

- Multiple BNPL plans across apps can sneak up on your budget. Each one feels small individually, but ₱1,500 a month here and ₱2,000 a month there adds up to a real chunk of your take-home pay. Track all of them in one place.

- A missed payment can affect your credit limit or future approvals on that app, even if there’s no formal credit bureau reporting (yet) for most BNPL providers in the Philippines.

Final Thoughts

None of these providers publish a single fixed rate that applies to everyone, and that’s the most important thing to understand before you use any of them. The published ranges in this guide tell you the boundaries, but your actual cost lives somewhere inside those boundaries, determined by your account and the specific offer in front of you. Use the typical-range calculator to compare broadly, then plug your real numbers into Part 2 once you have them. That’s the only way to know exactly what you’re signing up for.

Related Articles

Digital Bank Interest Calculator

SPayLater Calculator: Estimate Your Minimum and Maximum Cost

BNPL Cost Calculator: SPayLater vs LazPayLater vs BillEase vs Atome

How to Compute Holiday Pay, Overtime, and RD-OT (With Calculator)

Chinabank Rewards to Air Miles Calculator