A clear guide to MP2 early withdrawal rules, consequences, and what you should expect

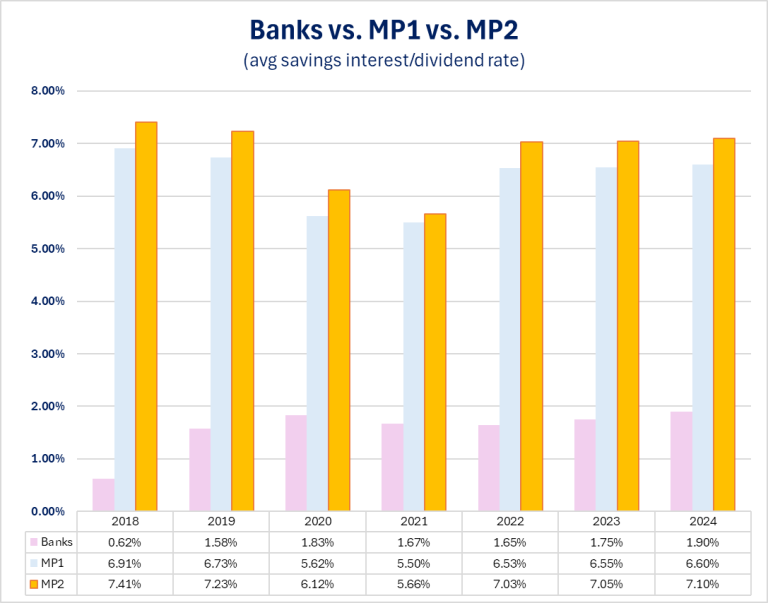

The Pag-IBIG MP2 Savings Program is one of the most popular ways for Filipinos to grow their savings. It’s a voluntary government-backed savings plan that typically earns much higher dividends than a regular bank savings account. But unlike a bank account, MP2 is meant to be held for a five-year maturity period, and withdrawing early can change how much you actually earn.

Let’s walk through what happens if you decide to withdraw your MP2 savings before those 5 years are up.

MP2 Pre-Termination/Early Withdrawal Calculator

Use this calculator to see how much you can get if you withdraw your Pag-IBIG MP2 savings early. Simply enter your principal, dividends already withdrawn, and dividends not yet withdrawn, then select the reason for withdrawal. The tool will show your total payout and how much you’ve earned so far.

If you are still unsure how to use this tool, read through the guide below to have a complete understanding of how MP2 early withdrawal works.

MP2 Early Withdrawal Calculator

- Valid reasons pay 100% of dividends not yet withdrawn.

- Voluntary withdrawals incur 50% dividend penalty applied to already withdrawn and pending dividends as described.

- This calculator is for estimation only. Actual Pag-IBIG MP2 payouts may vary.

What MP2 Is: Quick Recap

Before diving into early withdrawal, it helps to know how MP2 normally works:

- Five-year maturity: Your savings stay in MP2 for a full 5 years from the date of your first deposit. After this, you can withdraw both your principal (the money you put in) and your dividends (earnings).

- Dividends: MP2 dividend rates are declared annually and historically much higher than traditional savings accounts.

- You can choose to receive dividends annually or allow them to compound (roll into your principal).

Under normal circumstances, MP2 is designed to be a medium-term savings tool, not for frequent withdrawal or short-term emergencies.

For the complete guide on MP2, also read: High Dividends, Low Risk: Pag-IBIG MP2 Savings Program

Can You Withdraw MP2 Early? Yes, But There Are Conditions

Yes, the Pag-IBIG Fund allows you to withdraw your MP2 before the 5-year maturity, but how much you get depends on why you’re withdrawing.

There are two main scenarios as illustrated below:

| Scenario | Principal | Dividends Earned | Reason | Total Payout |

|---|---|---|---|---|

| Valid withdrawal | ₱200,000 | ₱30,000 | Critical illness | ₱230,000 |

| Voluntary withdrawal, compounded | ₱200,000 | ₱30,000 | Personal use | ₱215,000 |

| Voluntary withdrawal, annual payout | ₱200,000 | ₱20,000 (withdrawn) ₱10,000 (current year) | Change of mind | ₱195,000 |

Early Withdrawal for Valid Reasons

Pag-IBIG allows early withdrawal without the usual penalty if you have valid reasons as outlined in their T&C. For example, if you are diagnosed with a critical illness before the 5-year maturity period ended, you are qualified to withdraw 100% of your savings and the dividend earned.

The complete list of reasons honored by Pag-IBIG is as follows:

- Total disability or insanity

- Separation from work due to health issues

- Death of the member (beneficiaries can claim)

- Death of an immediate family member

- Retirement

- Permanent departure from the Philippines

- Unemployment due to layoff or company closure

- Critical illness of the member or immediate family (e.g., cancer, organ failure, heart issues; requires medical certification)

- OFW repatriation

- Other meritorious circumstances approved by Pag-IBIG

For example, if you contributed ₱200,000 and your account earned ₱30,000 over three years, withdrawing due to a certified critical illness would give you ₱230,000, full principal plus dividends.

Voluntary Withdrawal (50% Dividend Penalty)

If you withdraw MP2 early for reasons not listed above, the 50% dividend penalty applies. Your principal is never affected, but the dividends are reduced by 50%.

How the penalty works depends on your dividend choice:

- Compounded dividends: You receive only 50% of total dividends earned.

Example:- Principal = ₱200,000

- Dividends earned = ₱30,000

- Payout = ₱215,000

- Annual dividend payout: Any previously received dividends are deducted by 50% from your principal. Current-year dividends are also halved and released separately.

Example:- Principal = ₱200,000

- Previous dividends = ₱20,000 (withdrawn)

- Current-year dividends = ₱10,000

- Payout = ₱190,000 principal + ₱5,000 current-year dividend = ₱195,000

Withdrawals Before Dividend Declaration

Dividends are declared annually, so withdrawing before the first dividend declaration may result in little or no earnings, although your principal is always safe. MP2 is structured to reward time in the program, the longer you stay, the more you earn.

What Happens at Maturity

If you do not withdraw at the five-year mark, MP2 savings stop earning MP2 dividends. They earn Pag-IBIG I rates for the next 2 years, and after that, they are reclassified as accounts payable.

To continue in MP2 after maturity, you must open a new account.

Key Takeaways

Early withdrawal is allowed, but your principal is never penalized. Withdrawing for valid reasons preserves your dividends, while voluntary withdrawal reduces your earnings by 50%. The program works best when treated as a medium-term commitment. If you may need the money sooner, MP2 might not be the right place for all your savings. But if you can leave it untouched, the dividends make it worthwhile.

Related Articles

What Happens When You Withdraw Your Pag-IBIG MP2 Early (With Calculator)

MP2 Calculator

High Dividends, Low Risk: Pag-IBIG MP2 Savings Program

InstaPay vs PESONet: What’s the Difference and Which One Should You Use?

The Maya–Lazada and Maya–Grab Hack: Step-By-Step