With the boom in digital finance in the Philippines, savvy users are constantly finding ways to maximize rewards, stretch their budgets, and take advantage of platform ecosystems.

One strategy that has gained attention is the so-called “Maya–Lazada” and “Maya–Grab” credit card hack. While the term “hack” might sound technical or even illicit, what we’re really discussing here is a smart, strategic use of promos, cash-ins, and payment flows across platforms.

If done right, this can push your savings interest from 3.5% all the way up to 10% per year. This article breaks down how the method works, why people use it, and what you should consider before trying it yourself.

What Is the Maya–Lazada / Maya–Grab “Hack”?

This method focuses on triggering Maya’s bonus interest by increasing your total monthly spend.

Instead of relying only on real expenses, users route transactions through platforms like Lazada and Grab using their Maya wallet or card. These transactions count toward the required spend, helping unlock higher interest tiers.

In short, you use controlled transactions to boost your savings interest.

Why People Use This Strategy

The appeal is simple: higher returns on your savings.

- Maya gives a base 3.5% p.a. with no effort

- Spending unlocks additional bonus interest

- Reaching the highest tier can push your rate to 10% p.a.

For users keeping funds in Maya, that difference can be significant.

How It Works

The general flow looks like this:

- Use your Maya wallet or card for transactions

- Route spending through Lazada or Grab

- Accumulate total monthly spend

- Unlock boosted interest automatically

The main goal is to reach the highest spend tier (₱35,000 cash-in) to maximize your interest rate.

Step-by-Step Guide

Step 1: Prepare Your Maya Wallet

Make sure your Maya wallet has enough balance for your planned transactions. You can check here to see the boosted interest rate you can get for different cash-ins.

| Total Spend on Eligible Channels | Base Interest | Unlocked Bonus Interests | Ending Interest (p.a.) |

|---|---|---|---|

| ₱250 | 3.5% | 1.5% | 4.5% |

| ₱1,000 | 3.5% | 1.5% + 1% | 6% |

| ₱25,000 | 3.5% | 1.5% + 1% + 2% | 8% |

| ₱35,000 | 3.5% | 1.5% + 1% + 2% +2% | 10% |

Step 2a: Cash-in to your Lazada Wallet

- Open your Lazada app. Go to the LazFin section and click your wallet.

- Go to the Payment Options if you haven’t added your Maya card yet. You can link either your physical Maya card or your virtual card. Both card details are available in the Maya app.

- Once your card has been added, go to Cash-In. Input the amount.

- Proceed with the cash-in. If you see your Maya card in the options, use it. Otherwise, you may experience a common glitch where only the Maya e-wallet is available. In that case, choose Maya e-wallet. It works the same way as using the card.

- Double-check if the cash-in amount has been credited. Then, wait for the boosted interest rate to reflect in your Maya savings.

- You can then spend the money on Lazada, transfer it to another bank/e-wallet with a ₱15 fee, or just keep it in your Lazada Wallet. To maximize interest, we recommend transferring it to another high-yield digital savings platform. See your options here.

Step 2b: Cash-in to your Grab Wallet

- Open your Grab app and go to your GrabPay Wallet.

- Click Top-Up. Add your Maya card details under Cards. Using a Visa card is recommended because Grab charges an additional 2% for Mastercards.

- Once your card has been added, click on that card and input the cash-in amount. Click Confirm to finalize the transaction.

- Double-check if the cash-in amount has been credited. Then, wait for the boosted interest rate to reflect in your Maya savings.

- You can then spend the money on Grab, transfer it to another bank/e-wallet with a ₱15 fee, or just keep it in your GrabPay Wallet. To maximize interests, we recommend transferring it to another high-yield digital savings platform. See your options here.

Important Considerations

While the process is straightforward, there are a few things to keep in mind. First, the bonus interest only applies to up to ₱100,000 of your savings. Also, the cash-ins discussed in this article must qualify as valid spend. In practice, the Lazada method has been consistently reliable month after month, while some users report that Grab doesn’t always work as expected.

Everything resets monthly, so you’ll need to repeat these “hacks” each month. It’s best to do them at the start of the month to maximize your interest earnings. Lastly, always watch out for fees. They may seem small at first, but they can add up quickly, and that defeats the purpose of chasing higher interest rates.

Is It Worth It?

If you already keep money in Maya Savings, this strategy can be a simple way to boost your returns without changing much of your routine. At 10% p.a., it’s significantly higher than most digital savings accounts, which typically offer around 3%–4% p.a. Traditional bank savings can be even lower, sometimes below 1%.

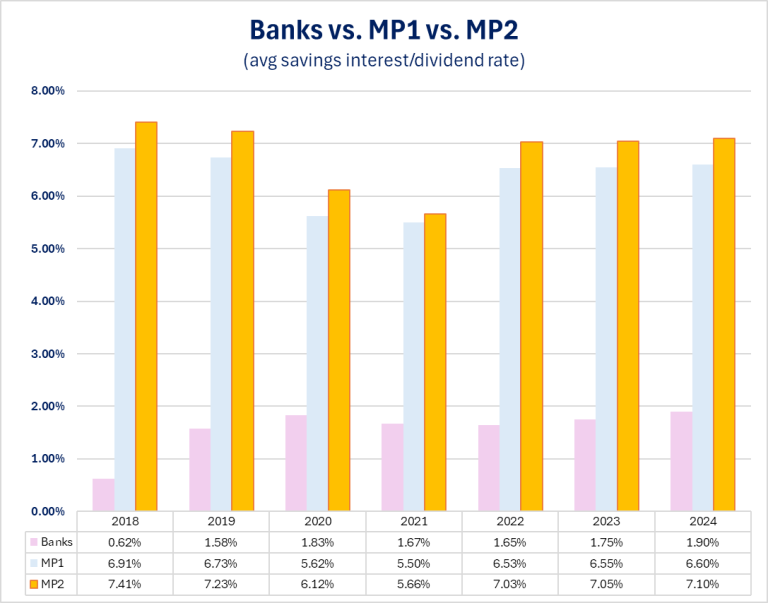

A close alternative is MP2, which offers around 7% annually, tax-free. You can check out our separate guide on MP2 to learn more.

The key is consistency. Once you understand the flow, it becomes a routine you can repeat every month.

Final Thoughts

The Maya–Lazada and Maya–Grab “hack” is really about understanding how Maya’s system rewards activity. By routing your transactions strategically, you can turn simple wallet activity into higher interest earnings, potentially reaching 10% per year on your savings.

For many users, that’s what makes this strategy worth exploring.

Related Articles

Maya Black vs Maya Landers Cashback Everywhere

Compounding Interest Explained: How Money Grows (With Calculator)

MariBank: Savings Interest Up To 3.75% (With Calculator)

Tonik Bank: Savings Interest Up To 6% (With Calculator)

High Dividends, Low Risk: Pag-IBIG MP2 Savings Program