Healthcare is one of the biggest financial risks for Filipinos. A single emergency can set a family back by ₱20,000 to ₱200,000, sometimes even more. Because of this, HMOs have become essential, not optional. They help protect your finances from unexpected medical expenses, whether that’s a sudden fever that requires lab tests or a week-long hospital stay due to dengue.

But with so many HMOs in the Philippines, choosing the right one can feel confusing. This article breaks everything down for you.

- What Exactly Is an HMO and How Does It Work?

- Why Having an HMO Is Important

- PH HMO Comparison Table

- HMO vs. Health/Medical Insurance

- Which Type of Member Are You? And What Plan Fits You?

- Major HMOs in the Philippines

- How Your Age Affects HMO Pricing

- What to Do If Your Hospital Isn’t Accredited

- How HMOs Work With PhilHealth

- How to Maximize Your Plan Before It Expires

- Why Preventive Care Saves You Money Long-Term

What Exactly Is an HMO and How Does It Work?

HMO is a healthcare provider that covers part or all of your medical expenses when you visit accredited hospitals and clinics. Think of it like a membership card for healthcare. You pay a yearly fee (called a premium), and in return, you get access to:

- Outpatient consultations

- ER treatment

- Diagnostics (X-rays, blood tests, ultrasounds)

- Hospital confinement

- Preventive care (APE, vaccines depending on plan)

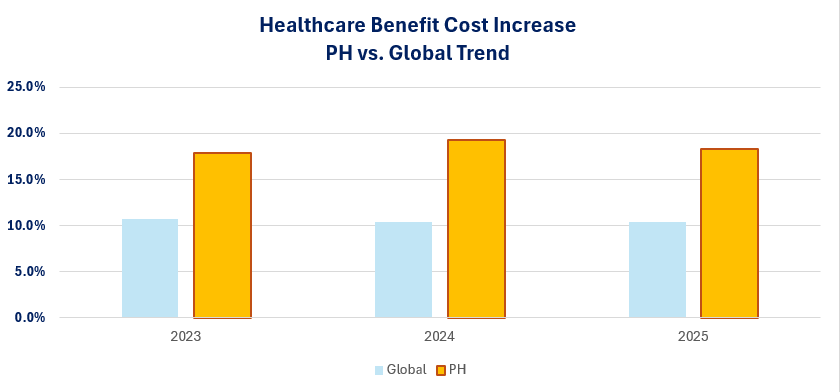

Why Having an HMO Is Important

Healthcare costs in the Philippines have increased significantly over the past decade. For the past three years, our healthcare‑benefit costs have climbed at a faster rate than most of the world, and this upward trend is projected to continue, according to the WTW Global Medical Trends Survey.

Even minor illnesses can drain your budget. A consultation costs ₱600–₱1,000, and multiple visits a year add up to a significant cost. Regular lab tests cost thousands too, what more for emergency cases and hospitalization?

PH HMO Comparison Table

To help you navigate your options, use this comparison table that gives you a clear, side-by-side look at the most important features of major HMOs in the Philippines, including premiums, coverage limits, room and board, emergency care, outpatient benefits, and more. Instead of checking each provider separately, this table puts all the essential details in one place so you can easily spot which plan best matches your budget, medical needs, and preferred hospitals.

| Features | Maxicare | Medicard Standard | Medicard VIP | Kwik Care | Pacific Cross Select Standard | Pacific Cross Select Plus | Pacific Cross Blue Royale | AXA HCA Lite | AXA HCA Prime | AXA Global Health Access |

|---|---|---|---|---|---|---|---|---|---|---|

| Annual Premium | ₱18,600–₱47,300 | ₱10,700–₱21,900 | ₱25,300–₱66,900 | ₱995–₱2,995/mo | ₱10,300–₱15,800 | ₱10,800–₱22,100 | $1,800–$3,600 | Upon Request | Upon Request | Upon Request |

| Coverage / Max Benefit | ₱100k–₱200k/yr | ₱50k–₱100k/yr | ₱200k–₱500k/yr | ₱50k–₱350k/yr | ₱1M–₱2M per disability | ₱1M–₱5M/yr | $500k–$2M/yr | ₱500k–₱5M/yr | ₱500k–₱5M/yr | ₱50M–₱175M/yr |

| Room & Board | Semi-private to Large Private | Ward to Small Private | Regular Private to Suite | Regular Private | Ward to Private | Ward to Private | Private Room | Private to Executive Suite | Private to Executive Suite | ₱7,500–₱125,000/night |

| Emergency Care | Covered + 80% non-accredited | Covered + 80% non-accredited | Covered (local & foreign) | Covered (local) | Covered (local & intl, ₱50k limit) | Covered (local & intl, ₱50k limit) | Covered (local & intl) | Local + up to 180 days intl | Local + up to 180 days intl | Local + up to 180 days intl |

| Out-Patient Check-Ups | Covered | Covered | Covered | Covered | Optional Add-On | Optional Add-On | Included (higher tiers) | Optional Add-On | ₱25k–₱125k | 90 days pre/post hospitalization |

| Labs & Diagnostics | Covered | Covered | Covered | Covered | Optional Add-On | Optional Add-On | 80% reimbursement (basic) | Optional Add-On | ₱25k–₱125k | 90 days pre/post hospitalization |

| Annual Physical Exam | Basic APE | Basic APE | Executive APE | Excluded | Executive APE | Executive APE | Executive APE | Basic APE | Basic APE | Executive APE |

| Dental | Optional | Covered | Covered | Excluded | Optional | Optional | Optional | Optional | Covered | Included (higher tiers) |

| Pre-Existing Conditions | Excluded (case review) | Covered from 2nd year | ₱5k–₱20k | 50% MBL after 6 mos & 100% MBL after 2 yrs | Covered from 2nd year | Covered from 2nd year | Excluded (case review) | Excluded (case review) | Excluded (case review) | Excluded (case review) |

| International Access | Emergency only | Emergency only | Covered | Excluded | Emergency only | Emergency only | Covered | Excluded | Excluded | Covered |

| Insurance Included | Life + Accidental | Excluded | Excluded | Excluded | PA + Travel | PA + Travel | Travel + optional PA | Life + Accident + Health Fund | Life + Accident + Health Fund | Excluded |

| Accredited Hospitals | View List | View List | View List | View List | View List | View List | View List | View List | View List | View List |

HMO vs. Health/Medical Insurance

Many Filipinos think they’re the same, but they aren’t. Understanding the difference helps you avoid gaps in your healthcare coverage.

- HMO (Everyday Care): Ideal for frequent but smaller expenses such as ER visits, checkups, diagnostics, and hospitalization with certain limits. HMOs are accredited-network based. This means you must go to hospitals that they’ve partnered with.

- Health Insurance (Big Medical Protection): Health insurance steps in when you face major illnesses like cancer, stroke, or heart disease. Most health insurance gives you a lump sum (like ₱500,000 or ₱1 million), which you can use however you want, even for treatment outside their network.

The best setup is to have both. An HMO handles the “small but frequent” expenses, while insurance covers the “rare but financially devastating” ones.

Which Type of Member Are You? And What Plan Fits You?

Not everyone needs the same kind of plan. Here are typical Filipino healthcare profiles:

- Young Professional: You’re probably healthy, but you get sick occasionally with flu, colds, stomach issues. Most of your expenses come from outpatient visits and diagnostics. You’ll want strong outpatient coverage, teleconsults, and affordable premiums.

- Family-Oriented Parent: Parents need pediatric care, easy access to specialists, and a high inpatient limit for kids. You’ll want pediatrician access, lab tests and diagnostics, dental options, and high room & board limits.

- Freelancer / Self-Employed: You don’t have employer-provided HMO, so your personal plan must be reliable and budget-friendly. You’ll want comprehensive individual plan, affordable monthly or annual payment, and good outpatient & emergency coverage

- Frequent Traveler or OFW: If you move in and out of the country, you’ll want international coverage. You’ll want worldwide hospitalization, global specialists, and high benefit limits

Major HMOs in the Philippines

Below is a deeper dive into how each HMO works, including real-world scenarios where each one excels.

1. MediCard

MediCard is one of the most established HMOs and is often praised for its lifestyle centers. These clinics cater specifically to their members, making outpatient services faster and more convenient.

What MediCard is known for:

- Highly flexible annual benefit limit

- Reimbursement options for non-accredited hospitals

- Option to pair with life insurance

- Useful for those who want more customization

2. Maxicare

Maxicare is arguably the most recognized HMO in the PH due to its digital services and large network.

What Maxicare is known for:

- Very strong outpatient and preventive coverage

- One of the biggest accredited networks

- Easy teleconsults

- Fast approvals via app

3. AXA

AXA leans toward the high end of the market, offering hybrids of HMO and health insurance. They also offer worldwide health care access in their GHA plan, which offers high coverage and worldwide treatment coverage.

What AXA offers:

- Worldwide treatment coverage

- Very high annual limits

- Access to global specialists

- Great for OFWs, expats, business travelers

- Longevity health funds

4. Pacific Cross

Pacific Cross is popular for inpatient-focused plans and travel-friendly benefits.

What Pacific Cross is known for:

- Strong hospitalization coverage

- Good customer service

- Popular among expats

- Travel insurance

- Good flexibility for pre-existing conditions (depending on plan)

How Your Age Affects HMO Pricing

The older you get, the higher your HMO premium becomes. This is because age increases the likelihood of illness, maintenance meds, and hospital visits. For example, a 25-year-old might pay ₱12,000/year for a plan, while a 55-year-old could pay double for the same coverage. This is why many people lock in an HMO while they’re young, renewal rates usually increase gradually instead of jumping sharply.

What to Do If Your Hospital Isn’t Accredited

If your preferred hospital is not accredited, you still have options. Depending on your HMO plan, you can use reimbursement, but this means paying the hospital bill upfront and filing documents afterward.

Some people choose to keep their main HMO and add a secondary plan that includes their preferred hospital. It’s also possible to ask the HMO which accredited facility near your preferred hospital offers similar services, sometimes it’s just one street away.

How HMOs Work With PhilHealth

HMOs and PhilHealth share the cost of your hospital bill. PhilHealth usually covers a fixed amount, and the HMO pays the rest based on your plan’s limit. This means you get smaller out-of-pocket expenses.

Note that most, if not all, HMOs require their members to have an active PhilHealth membership. Otherwise, the member must pay the PhilHealth portion out of pocket before the HMO takes effect.

How to Maximize Your Plan Before It Expires

Before your HMO renews, use the benefits you’ve already paid for. Many plans include annual physical exams, dental cleaning, or routine consultations that people forget to use. A quick checkup before renewal can catch issues early and avoid bigger medical bills later. It also lets you assess if your current plan still fits your needs or if you should upgrade or downgrade.

Why Preventive Care Saves You Money Long-Term

Preventive care like checkups, screenings, and vaccines helps detect problems early before they become expensive illnesses. For example, a simple annual blood test might catch high sugar levels before it turns into diabetes, saving you years of medication and hospital visits. HMOs usually cover these routine services at no added cost, making them some of the most financially valuable benefits you can use.

Related Articles: